Description

What the strategy is actually betting on

An ITM covered call combines 100 shares or ETF units with a call sold at an in-the-money strike. That immediately brings in premium while reducing the net entry basis somewhat.

The real thesis is not an aggressive bullish view. The core assumption is that the extrinsic value of the short call decays. In practice this makes the trade a theta setup first and foremost, with time decay doing the heavy lifting.

Strike selection should follow one hard rule here: the chosen strike should sit below the expected move for that expiration cycle. That keeps the position inside a reasonable volatility envelope instead of requiring an unusually large directional move.

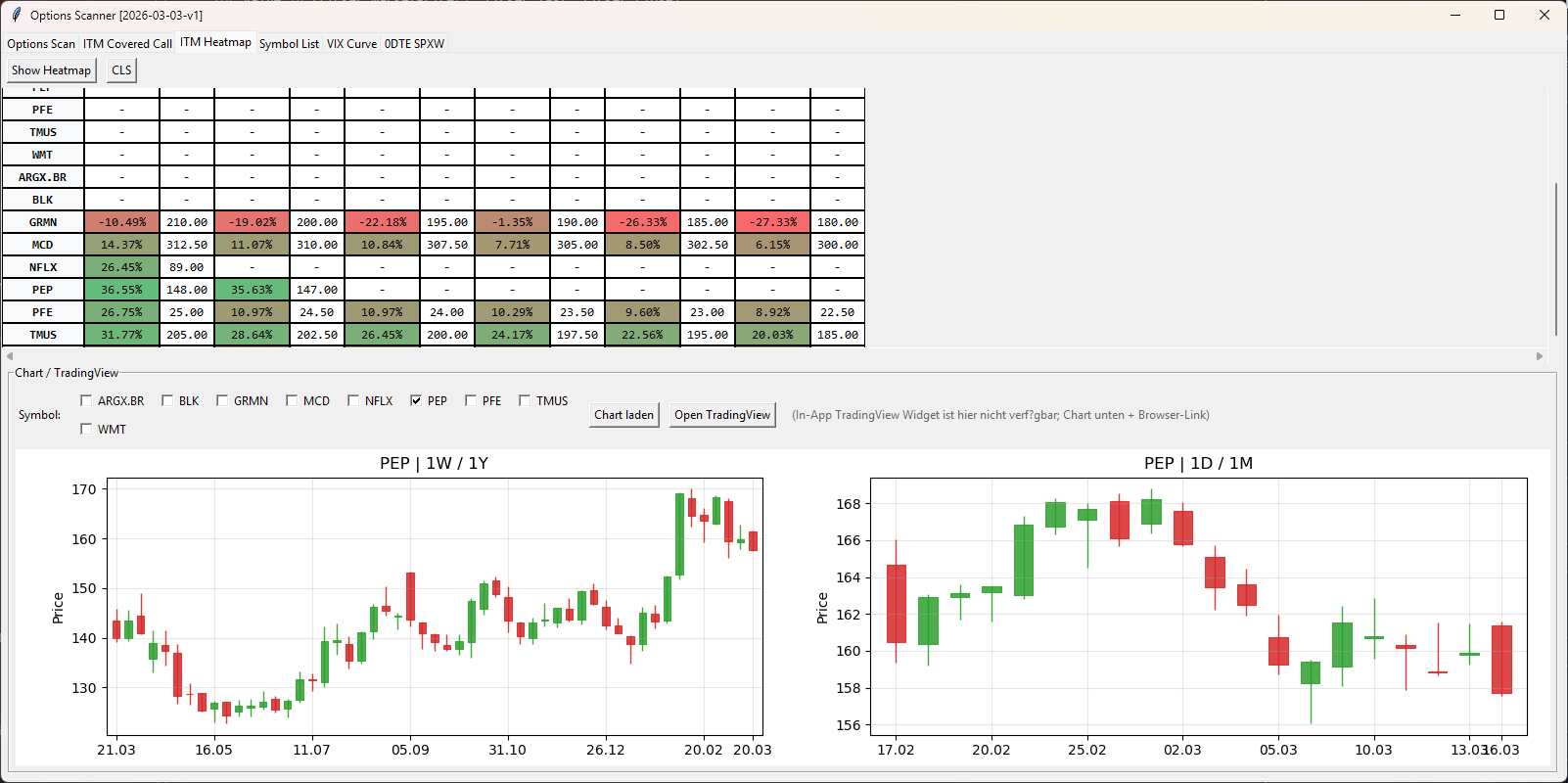

To justify the capital usage and friction, the annualized return should in our view be at least 20%. You can run a live scan for candidates directly in the Optionist.net OWS Tools.

One of the clear drawbacks is the lack of meaningful upside. If the underlying rallies hard, you do not properly participate in that additional move because the short call caps the profit on the upside.

If the stock falls materially and finishes below the strike into expiration, there are three clean paths: roll the position and sell a new ITM call, sell the underlying outright, or manage the trade earlier with a defined exit. One practical framework can be an exit stop around 10% in the underlying so the loss is realized intentionally instead of drifting further.

- Underlying Prefer liquid, steadier stocks or ETFs over unstable high-beta names.

- Tenor Short-dated cycles keep the theta component in focus.

- Strike logic The ITM strike stays below the expected move of the cycle.

Example: MSFT

Assume Microsoft trades at 395.55 USD and the expected move for 14 DTE is 20 USD. A short call at 370 USD can then serve as the example setup.

- Spot to strike distance 395.55 minus 370.00 = 25.55 USD of intrinsic value.

- Call premium Assume 28.00 USD.

- Pure time value 28.00 minus 25.55 = 2.45 USD per share, or 245 USD per contract.

- Annualized 2.45 / 370.00 = 0.662% for 14 days. Multiplying by 252 / 14 gives roughly 11.9% per year.

This example isolates the theta component cleanly, but at roughly 11.9% annualized it still falls below the 20% yearly target and therefore would not be an ideal candidate.

A scan for suitable stocks and ETFs can be run with the OWS tool. The included heatmap helps estimate whether a position is worth taking.

Inspired by: Theta Profits, In The Money Covered Call.